National News Australia

Breaking records and breaking hearts – Australian Winter Crop Forecast

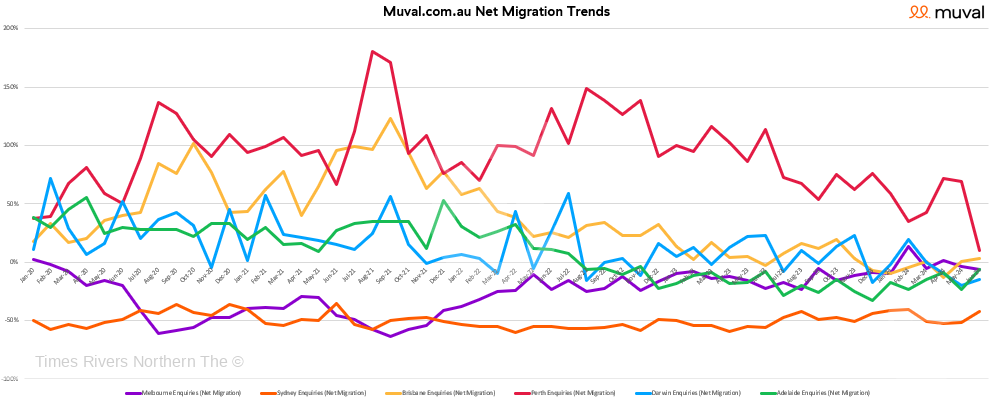

Muval migration data for the first six months of 2024

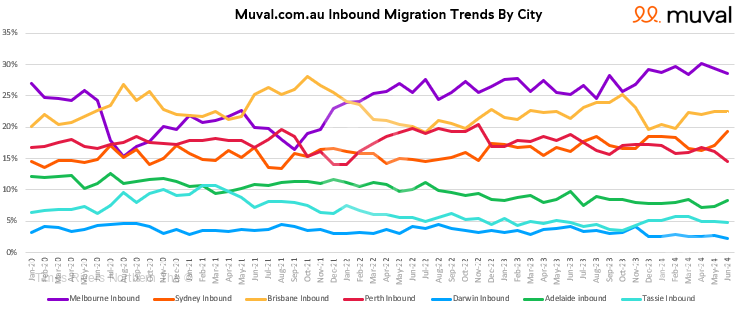

According to national online removalist booking platform Muval, which has the most up-to-date internal migration data showing where Australians are moving, Melbourne is the number one capital to move to in the first half of 2024, with inbound traffic peaks in February and April catapulting the city into positive net migration for the first time since before COVID.

The latest moving data also shows that rising cost of living pressures continue to take their toll on Sydney and increasingly Brisbane, with the river city dipping as low as -13% into negative territory this year.

While rental moves are traditionally local, within the same suburb or neighbouring suburbs, Australians aren’t hesitating to cross borders in search of more affordable housing, more lucrative work or a cheaper lifestyle to maintain their current living standards.

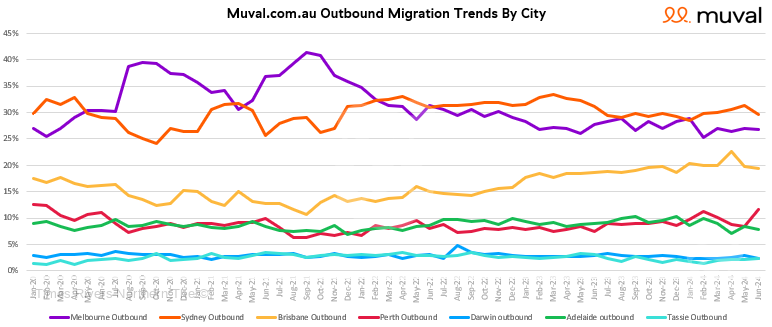

With that said, industry-wide moving numbers are down around 20% on the same time last year. Overall, Muval reports that the current macro-economic climate of higher interest rates, tight housing affordability and housing shortages are having a cooling effect on moving generally.

As people typically enquire about removalist up to 30 days before they move, Muval’s data is a proven early indicator of moving trends in Australia.

Muval – Net Migration June 2024

Melbourne

For the first time since January 2020, Melbourne entered positive net migration in 2024. Off the back of a rise in inbound moves (30% of all major metro moves were to Melbourne in February and April) and a fall in outbound moves, down to 25% of all major metro moves in February which is the lowest on record, the city finally slipped back into positive territory with +13% net migration in February and +2% in April. The last time the city had positive net migration was before the pandemic (+3% Jan 2020) and it fell as low as -61% in August 2020 and -64% in September 2021 when thousands fled lockdowns in the city. When Melbourne’s outbound enquiries veered down, Brisbane and Sydney’s spiked, suggesting the traffic is flowing down from the increasingly expensive northern states.

Muval – Outbound June 2024

Brisbane

A rise in the cost of living in Brisbane, including skyrocketing housing prices up more than 60% since the onset of COVID and a rise in unit rentals of more than 50%, is affecting the city’s appeal as a place to live. Brisbane’s outbound moving enquiries have jumped to their highest level, reaching 23% of all major metro outbound moves in April. Averaging 22% of inbound metro moves in the first six months of the year, Brisbane came close to Sydney when it dipped to just 20% in January and February (Sydney accounted for 19% and 18% respectively). After peaking at +123% positive net migration in September 2021, Brisbane teetered around zero in the first six months of this year before tumbling to a record low of -13% in April. While it remains the second most popular city to move to behind Melbourne, Brisbane’s pandemic popularity has been replaced with an air of unaffordability.

Muval – Inbound June 2024

Sydney

Sydney has experienced a slight increase in inbound traffic during the first six months of this year, accounting for as much as 19% of all major metro inbound moves in January and June (the highest number on record for Sydney), to cement its place as the third most popular city to move to. This is a change from last year when Perth was third behind Melbourne and Brisbane. With an average of 30% of all major metro outbound moves coming from Sydney in the first six months of 2024, the Harbour City continues to boast the unfortunate title of biggest resident exodus. While there are glimmers of hope, this outbound movement has kept Sydney firmly in negative net migration between -41% and -52% in the first half of the year.

Perth

For the first time in years, Perth appears to be losing its strong grip on positive net migration. It is still the highest in the country, but it’s spiralling fast to pre-pandemic levels as interest in the state tapers off, perhaps as rents rise at a record rate. Perth saw the highest annual rent increase of all capital cities in the last year (up 14 per cent year-on-year), as well as the highest rise in rent values since the onset of the pandemic at nearly 60 per cent. After a 2021 pandemic peak of +181%, net migration dropped to +10% in June, off the back of low inbound traffic of just 14% and high outbound traffic of 12%. Perth hasn’t had outbound traffic consistently in double digits since the start of 2020, it sat between 7-9% in 2022 and 2023.

Adelaide

After consistently sitting around 9-10% in 2023, Adelaide’s outbound migration appears to be slowing in the first six months of 2024, dipping as low as 7% in April and staying on 8% in May and June. However, inbound traffic hasn’t picked up this year and at 7% in April and May, it’s Adelaide’s lowest share of inbound major metro moves on record. After entering negative territory in August 2022, the city remains in negative net migration in 2024 hovering between -7% (June) and -23% (February and May).

For more information visit muval.com.au

For more real estate news, click here.

The Northern Rivers Times Newspaper Edition 224

Council decides not to appeal Iron Gates ruling

Growers demand commitment on power prices and insurance

Temporary Road Closures Byron St and Ross St, Lennox Head

Labor’s vaping prohibition is resulting in more crime

Unlawful Merchant Fees Charged to Customers

A NEW TWEED HEADS

Toyota Supra: Get Ready For A Fully Electric Version In 2025

Northern Rivers Local Health District COVID-19 update

Northern Rivers COVID-19 update

Fears proposed residential tower will ‘obliterate’ Tweed neighbourhood’s amenity and charm

COVID-19 Vaccination Clinic now open at Lismore Square

Muval migration data for the first six months of 2024

Muval migration data for the first six months of 2024 According to national online removalist booking platform Muval, which has...

Call for more mates to support Port Macquarie’s Sailability

Call for more mates to support Port Macquarie’s Sailability Vision available: https://tinyurl.com/mrz9nhz7 The Port Macquarie community group, Sailability, is calling...

Teen charged with multiple property offences in Cowra – Operation Regional Mongoose

Teen charged with multiple property offences in Cowra – Operation Regional Mongoose Tuesday, 24 September 2024 02:01:49 PM A teen...

-

Tweed Shire News2 years ago

Tweed Shire News2 years agoA NEW TWEED HEADS

-

Motoring News2 years ago

Motoring News2 years agoToyota Supra: Get Ready For A Fully Electric Version In 2025

-

COVID-19 Northern Rivers News3 years ago

COVID-19 Northern Rivers News3 years agoNorthern Rivers Local Health District COVID-19 update

-

COVID-19 Northern Rivers News3 years ago

COVID-19 Northern Rivers News3 years agoNorthern Rivers COVID-19 update

-

Northern Rivers Local News3 years ago

Northern Rivers Local News3 years agoFears proposed residential tower will ‘obliterate’ Tweed neighbourhood’s amenity and charm

-

Health News3 years ago

Health News3 years agoCOVID-19 Vaccination Clinic now open at Lismore Square

-

COVID-19 Northern Rivers News3 years ago

COVID-19 Northern Rivers News3 years agoLismore Family Medical Practice employee close contact

-

NSW Breaking News3 years ago

NSW Breaking News3 years agoVale: Former NSW prison boss Ron Woodham