Local News

Using super for house deposits increases property prices by $75,000

Using super for house deposits increases property prices by $75,000

Super Members Council

Allowing first homeowners to withdraw their super for a house deposit could see property prices rise by nearly $75,000 across Australia’s five largest capital cities, new modelling from the Super Members Council shows.

Pouring retirement savings into housing would inflame an already-inflated property market – pushing up the major capital city median price by an estimated 9%.

The Super Members Council (SMC) modelled a scheme that would allow a first home buyer to take $50,000 from their super for a deposit – as has been proposed.

The rigorous econometric model found the scheme fuelled demand in capital cities and led to price increases that quickly exceeded the $50,000 first homeowners could withdraw from super.

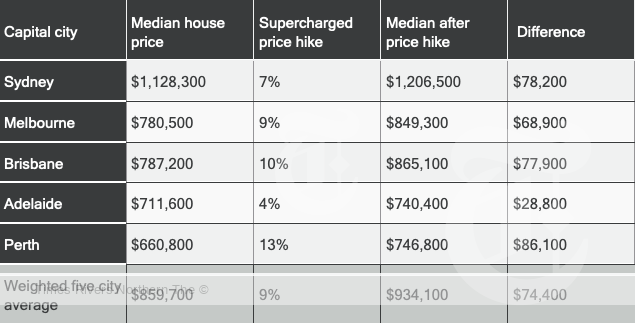

The model showed prices would hike in all capital cities, with the Sydney median ballooning by almost $80,000, in Melbourne by nearly $70,000, Brisbane by $78,000 and in Perth by a whopping $86,000. (See Table 1)

Super Members Council CEO Misha Schubert said allowing withdrawals from super for house deposits could raise prices for everyone – meaning all home buyers would pay higher mortgages for longer, exacerbating the cost-of-living crisis.

“Using retirement savings for house deposits would just unleash a huge price hike,” Ms Schubert said.

“That would mean higher and longer mortgages for Australians – and would quickly make capital cities even less affordable for new home buyers struggling to get into the market.”

“We all desperately want more Australians to own their own home, but this idea won’t achieve that – it would just make that goal even harder for first home buyers by making house prices even more expensive.”

Impact on capital city prices of allowing a first home buyer to withdraw $50,000 from super

Ms Schubert said a growing list of policy ideas that encourage people to raid their retirement savings come with long-lasting consequences for everyday Australians and the country.

“Breaking the seal on super leaves people poorer in retirement and costs every Australian taxpayer more from higher age pension costs.”

SMC analysis shows a 30-year-old couple who withdrew $35,000 each from their super could retire with about $195,000 less in today’s dollars. People retiring with less super increases age pension costs, which would likely be met by higher taxes – a price every Australian will pay.

Robust international studies confirm schemes that allow people to access retirement savings for house deposits do not lift rates of home ownership.

A Mercer study of its Global Pension Index found that countries that allow early access to retirement savings for housing did not have higher rates of home ownership than Australia.

The study also concluded the common feature of the best global retirement systems were that they ‘preserved’ savings until retirement.

An academic review of the New Zealand super scheme, Kiwisaver, that allows withdrawals for housing, found balances were far lower partly due to the country’s first home deposit withdrawal scheme. New Zealand also has a lower rate of home ownership than Australia.

A chorus of credible economists, Retirement Income Review author Mike Callaghan, the RBA, APRA, Coalition PM Malcolm Turnbull and OECD General Secretary Mathias Cormann have all cautioned using super for housing deposits could inflate property prices.

“The Super Members Council works with Parliamentarians and policy makers across the full breadth of the Parliament to ensure super policy is stable, effective and equitable,” Ms Schubert said.

“We produce rigorous research and analysis to help inform policy development that protects and promotes the interests of the 10 million everyday Australians we represent.”

For more real estate news, click here.